Photo by Thomas Winz / Getty Images.

America is, by and large, a nation of homeowners. Though more than 100 million Americans rent, they’re outnumbered two-to-one by Americans who own their own home, according to data from the U.S. Census.

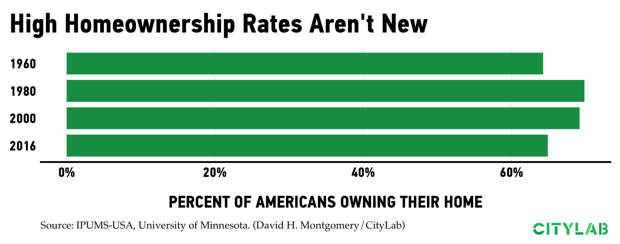

And that’s nothing new. Americans have had high rates of homeownership for a long time, with only modest changes over the decades:

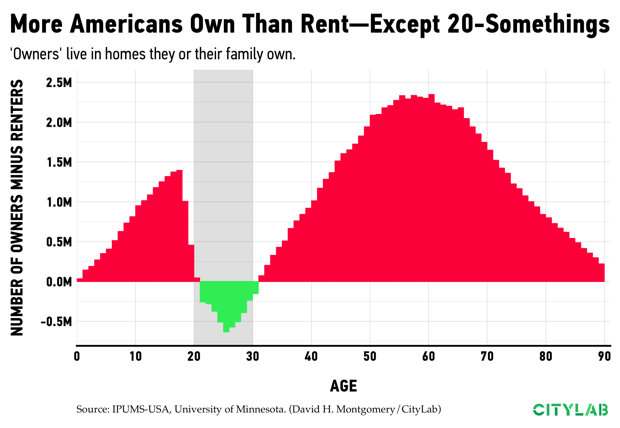

But the populations of homeowners and renters aren’t flat across the U.S. There’s one major group of Americans who are more likely to rent than own: people in their 20s.

Adults older than 30 are more likely to live in homes they own rather than rent, a likelihood that increases as they get older. Similarly, most children live in homes their parents own—though the youngest children are the most likely to live in rented housing.

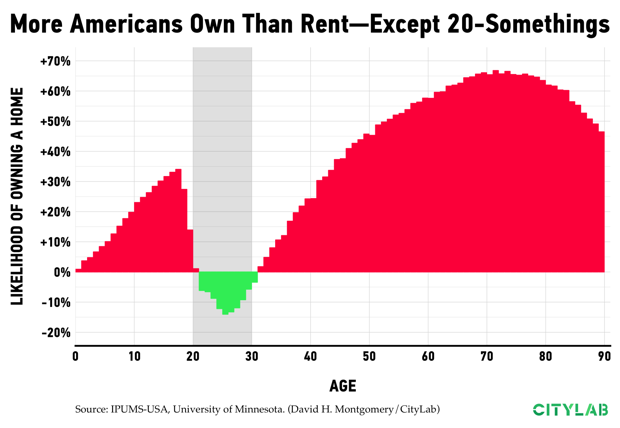

Here’s that same graph again, but as percentages instead of raw numbers. Looking at it this way makes clear that, for example, the elderly aren’t drastically more likely to rent—there are just fewer of them.

This trend isn’t very surprising—it takes capital to buy a house, something many 20-somethings lack. And people in their 20s can be more mobile and less likely to be married with children.

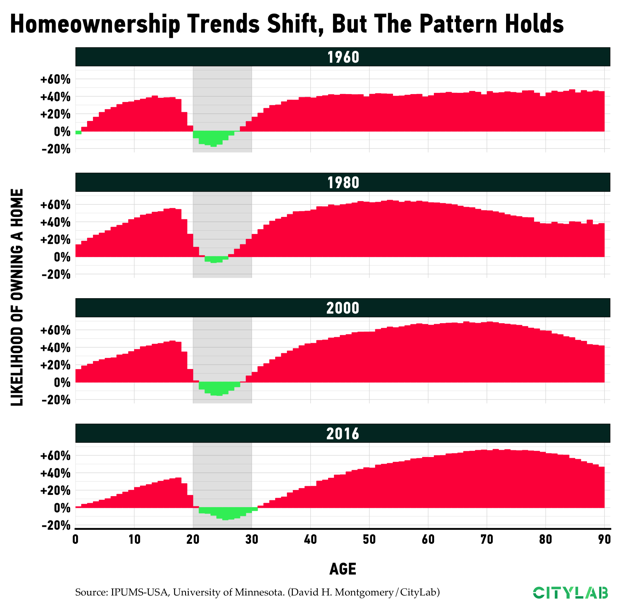

The trend has also remained relatively stable for decades. But there has been some change in the age when people shift from renters to owners. In 1980, for example, young-adult Baby Boomers were much more likely to own a home than today’s young-adult Millennials. Even then, though, the 20s were the only ages when renters sometimes outnumbered owners:

“The generation of people who are now in their 20s and early 30s are moving into home ownership at roughly the same rates the Baby Boomers did. They’re just starting later,” said Susan Brower, Minnesota’s state demographer. “The whole curve gets shifted to a later period in time.”

The trend of Americans renting in their 20s also holds steady when controlling for other factors that affect homeownership. For example, residents of cities are much more likely than rural Americans to rent, regardless of their age. But both areas see a rise in renting among 20-somethings:

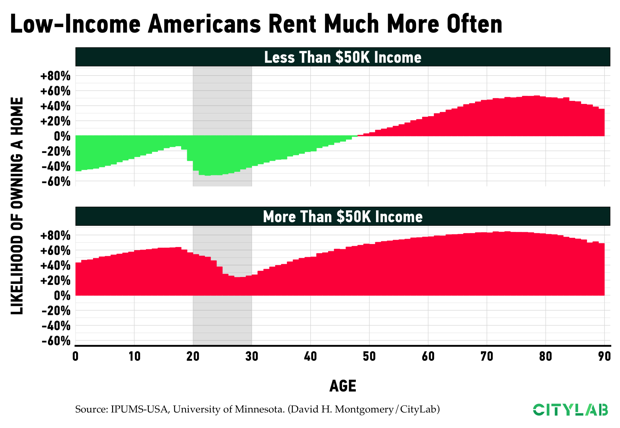

Similarly, lower-income Americans are much more likely to rent than wealthier Americans. Households earning less than $50,000 per year have a homeownership rate of around 45 percent, while nearly 80 percent of households earning more than $50,000 own.

The effect of income is drastic—but the shape of the pattern remains largely the same. In both rich and poor households, renting peaks in one’s 20s and falls steadily afterwards. The difference is that wealthy households are more likely to own than rent at all ages (they’re just least likely to own in their 20s). Lower-income Americans, meanwhile, don’t become majority-homeowners until nearly age 50. (One difference: the highest rate of renting among low-income individuals is in their early 20s, while renting maxes out among higher-income Americans in their late 20s.)

Kids in lower-income households typically live in rented housing, while richer kids tend to live in homes their parents or guardians own.

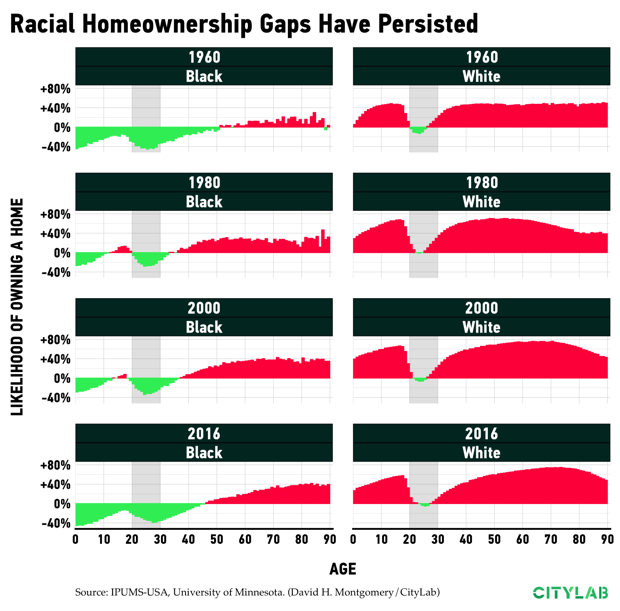

In addition to income, the Census data shows a pretty big homeownership gap based on race. Hispanic and black Americans own homes at significantly lower rates than do white and Asian/Pacific Islander Americans. That's in line with other studies, such as a recent Harvard study finding 43 percent of black adults own homes compared to 72 percent of white adults.

Some, but not all, of this disparity is tied up with income. The median household income for black Americans is less than $40,000 per year, compared to more than $60,000 for white Americans. The Census data shows a relationship between homeownership and both race and income. Low-income households of all races are more likely to rent. But black households are less likely to own homes than white households in similar income bands:

The racial gap in homeownership has persisted over the decades. But in 2016, blacks were less likely to own homes at nearly every stage of life than they were in 2000 or 1980:

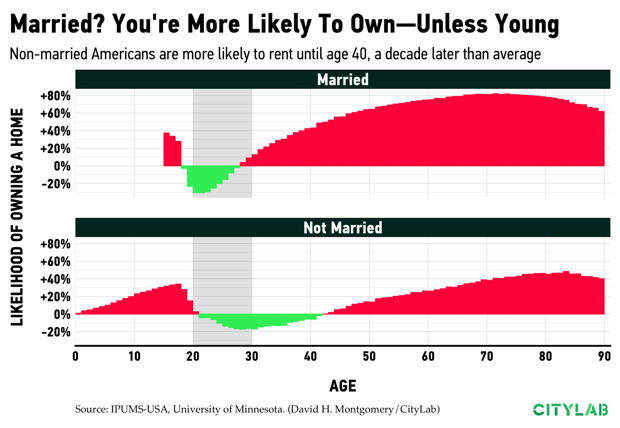

Marriage is also statistically linked to homeownership, with married individuals overwhelmingly more likely to own homes.

But the trend here is a little different. Americans who marry in their early 20s—well below the country’s median age at first marriage of around 28 for men and 26 for women—are actually more likely to rent than their single brethren.

Meanwhile, Americans who don’t marry break the trend of becoming homeowners in their 30s. Unmarried individuals are more likely to rent than own past age 40:

Turning to the oldest population of owners, one other thing has changed since the 1960s. Then, homeownership rates peaked around age 40 and stayed constant for older Americans, neither rising nor falling. Data from 1980, 2000, and 2016, on the other hand, show a curve with a peak and then a decline—though the age of peak homeownership has gotten later and later. This reflects many Americans moving in their 70s and 80s out of homes they own, whether because they choose to rent a more manageable apartment or move to assisted living facilities. See below how homeownership rates have declined among older Americans in recent decades.

This analysis is based on random samples of responses from the 1960, 1980, and 2000 U.S. Censuses, and the Census’ 2012-2016 American Community Survey. The combined dataset includes more than 22 million responses over the four time periods. Data was downloaded from the IPUMS-USA database at the University of Minnesota.